Global Perspectives

The world in 2026 doesn’t feel like a world in transition. It feels like a world that’s already transitioned. The assumptions that underpinned the post-World War II order are quietly being retired. The demographic engines that sustained the West’s prosperity are slowing in plain sight. Technologies once framed as tools to augment human work are now beginning, subtly but decisively, to reorganize it—in ways most institutions are not yet structurally equipped to manage.

This project rests on a simple conviction: the trends shaping the next decade are already visible. But more than most years, 2026 demands a macro, interconnected, and genuinely global lens: only by tracing the links between systems can we see the forces shaping tomorrow. We identified eight of them.

Some are technological. Others are demographic, geopolitical, industrial, or cultural. But these labels matter less than the patterns they reveal. Taken together, they describe a broader reconfiguration of how power is distributed, legitimacy is constructed, and value is created. These shifts do not move in parallel; they interact. Energy constraints shape industrial strategy. Demographic shifts reshape capital flows. Technological capabilities pressure governance. Cultural momentum anticipates economic realignment. Understanding them requires synthesis: the ability to perceive connections before they are obvious.

Each section blends narrative with data and curated readings for those who want to know more. The eight trends highlighted here are not exhaustive; they’re the ones we consider most structurally consequential, the clearest indicators of the direction of travel.

Data Centers Will Be Everywhere

From India to Australia, everywhere seems fit for a data center. Some would argue: even space.

Every time you ask an AI a question, somewhere a building the size of several city blocks consumes enough electricity to power thousands of homes—just to give you your answer. Now multiply that by billions of requests per day, and you begin to understand why data centers have become the most contested infrastructure of our time.

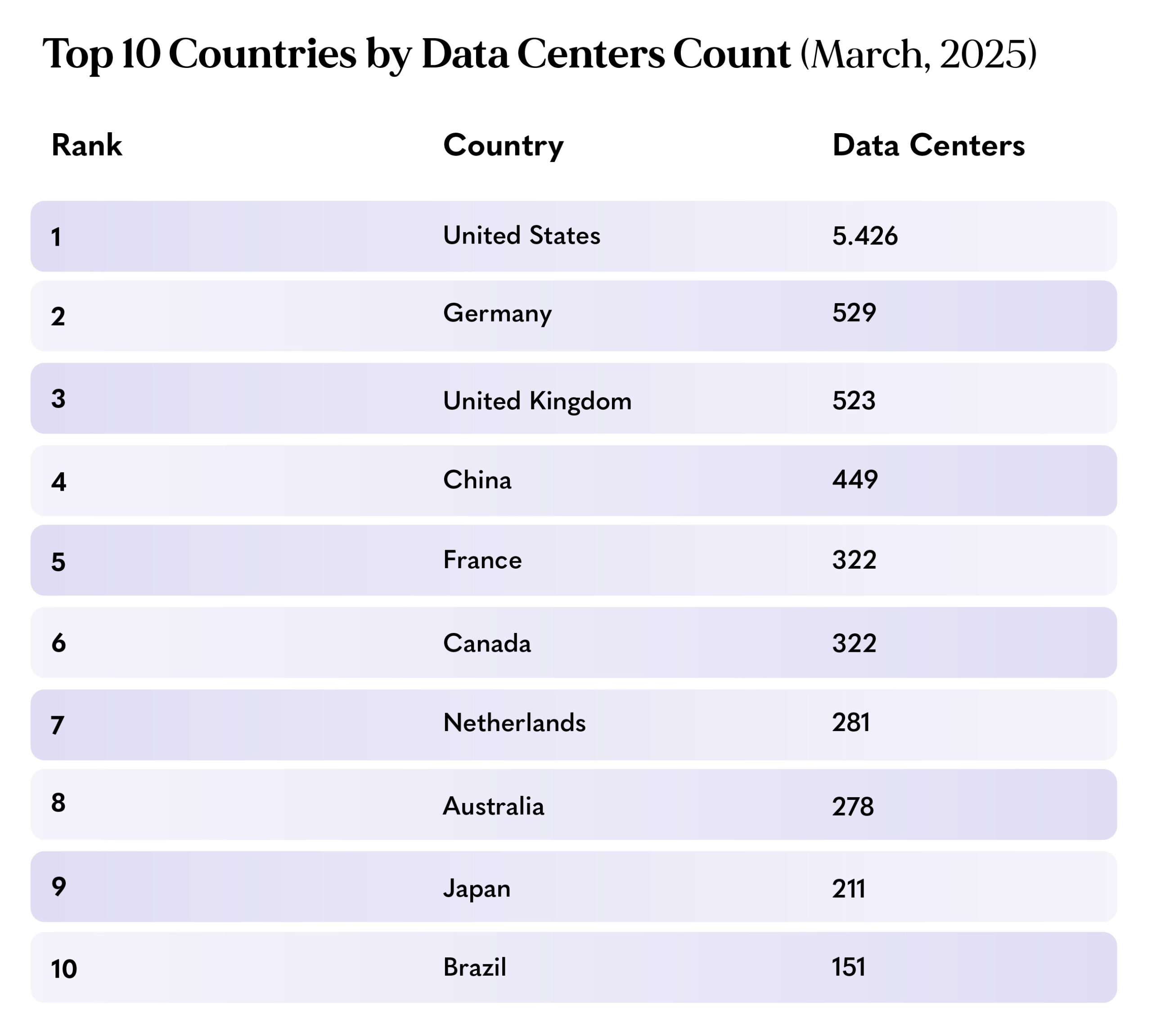

There are nearly 9,000 operational facilities worldwide today; by 2030, that number will triple. The reason is simple: AI runs on computing power, computing power runs on data centers, and every country wants both on its own soil.

Source: DCPulse

India is mandating local data storage for national security. Saudi Arabia and the UAE struck $600 billion in AI infrastructure deals with the U.S. in 2025 alone. Australia is fast-tracking what could become the world’s largest single facility—an entire gigawatt-sized campus outside Sydney that would consume almost half the output of a full coal plant.

The core tension, though, is geographical: data centers work best in cool, water-rich environments, yet demand is pushing them into hot, water-scarce places like Singapore, Indonesia, and Nigeria, where cooling costs more energy and strains local grids. This pressure is forcing a choice—and creating an opportunity. On one side, the temptation to build fast and ask questions later. On the other, a genuine acceleration in sustainable cooling research: direct-to-chip liquid systems, immersion cooling, seawater-cooling pilots, even proposals to move processing capacity into orbit, where solar energy is constant and heat dissipation free.

Whether that’s innovation or desperation, 2026 will begin to provide an answer.

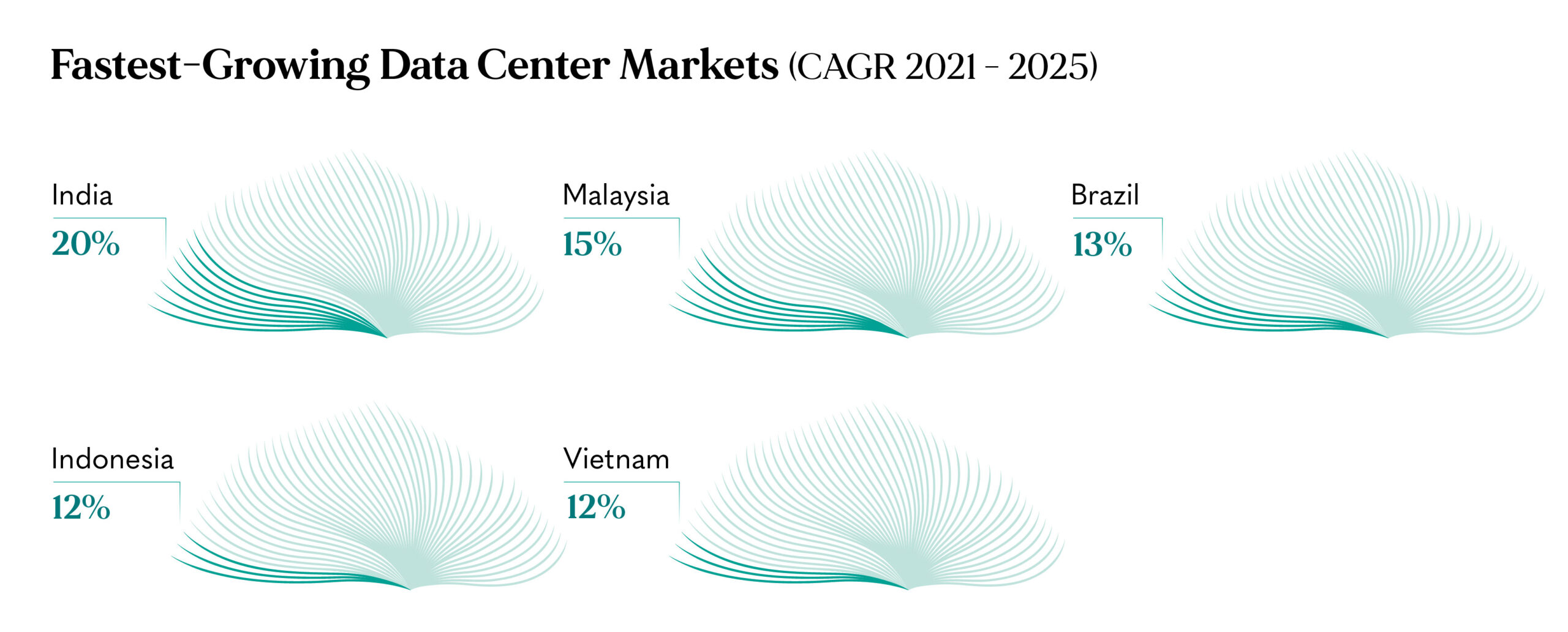

Source: DCPulse

Imminent selection of global sources to dive deeper into the issue:

Green Is Hot (Again)

With major Chinese investments and many countries following suit, this could be the year green becomes unstoppable.

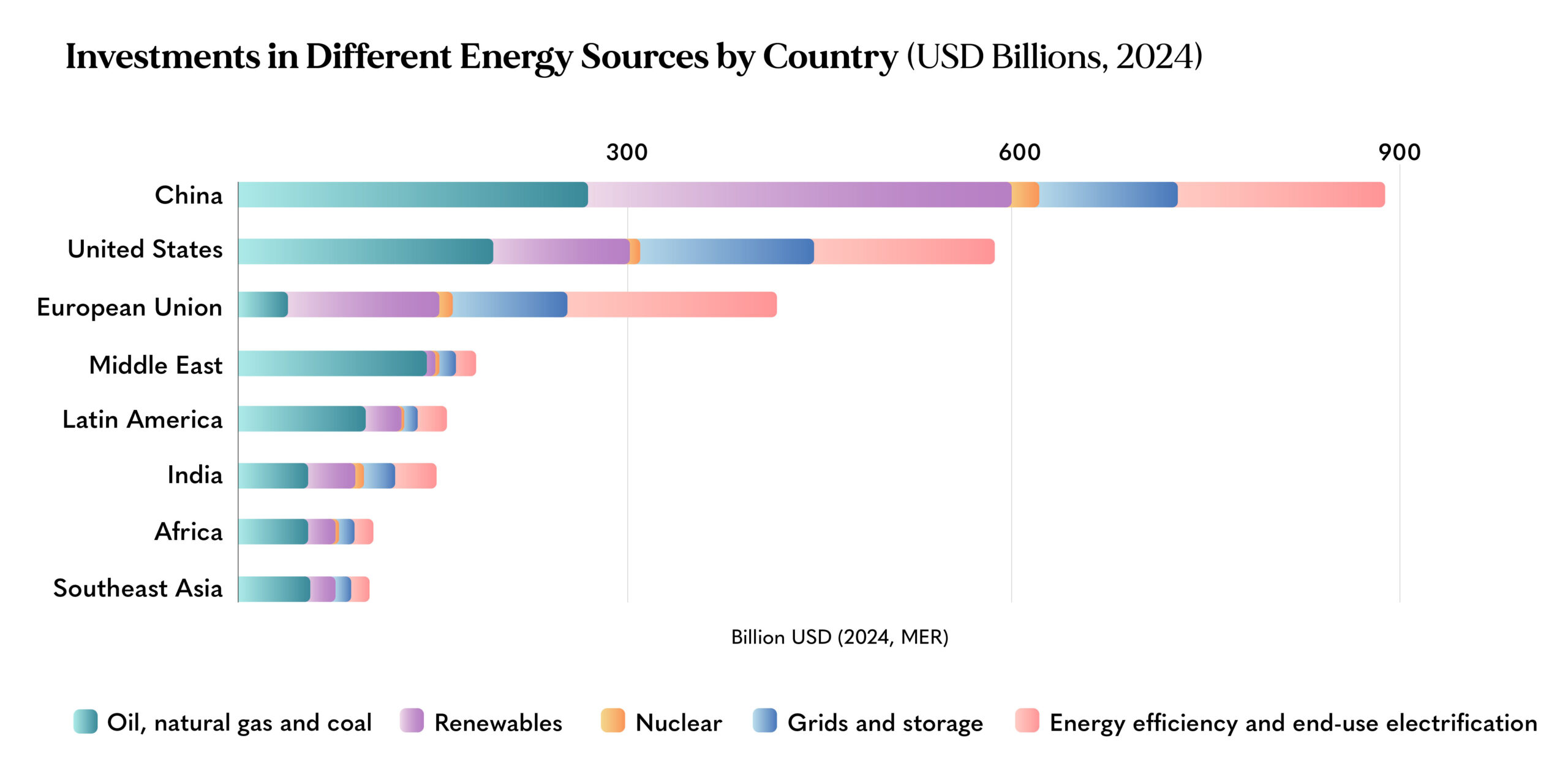

Donald Trump pulled the USA out of the Paris Agreement for the second time, yet clean energy has never moved faster or attracted more money. Global energy investment hit $3.3 trillion in 2025, with two-thirds flowing into clean technologies: renewables, batteries, grids, and EVs. The transition didn’t slow down. It changed language.

China is the clearest proof of this: its clean energy sectors generated a record $2.2 trillion in output last year, more than the entire economy of Brazil, and accounted for over 90% of the country’s investment growth. In early 2025 alone, China added 240 gigawatts of new solar capacity, more than the entire world installed in 2023. Solar is now set to overtake coal in China for the first time in 2026.

But this is no longer just a Chinese story. In Indonesia, Chinese and local companies are working together to build the country’s first large-scale integrated solar manufacturing plant. In Brazil and Chile, abundant renewables are attracting investment in data centers that a decade ago would have gone to Europe. In Scotland, China’s largest private manufacturer of wind turbines is seeking to establish a manufacturing presence, though it faces significant political resistance over concerns around energy security—a tension that itself reveals how crucial clean energy has become to geopolitical competition. India, meanwhile, is planning to bring online a massive complex to house gigafactories for solar panels, batteries, and electrolyzers.

The economics are now self-sustaining: solar provides what the IEA calls “the cheapest electricity in history,” and in much of the Global South, going renewable is simply about the bottom line. What makes this moment different is that green is no longer driven by climate consciousness—it’s driven by industrial competition, energy sovereignty, and the race to control the supply chains of the future. That may be precisely what makes it, finally, unstoppable.

Source: World Economic Forum

Imminent selection of global sources to dive deeper into the issue:

Unexpected and Uncertain

Someone has shown the world that this order is not inevitable after all. Markets may pay the price.

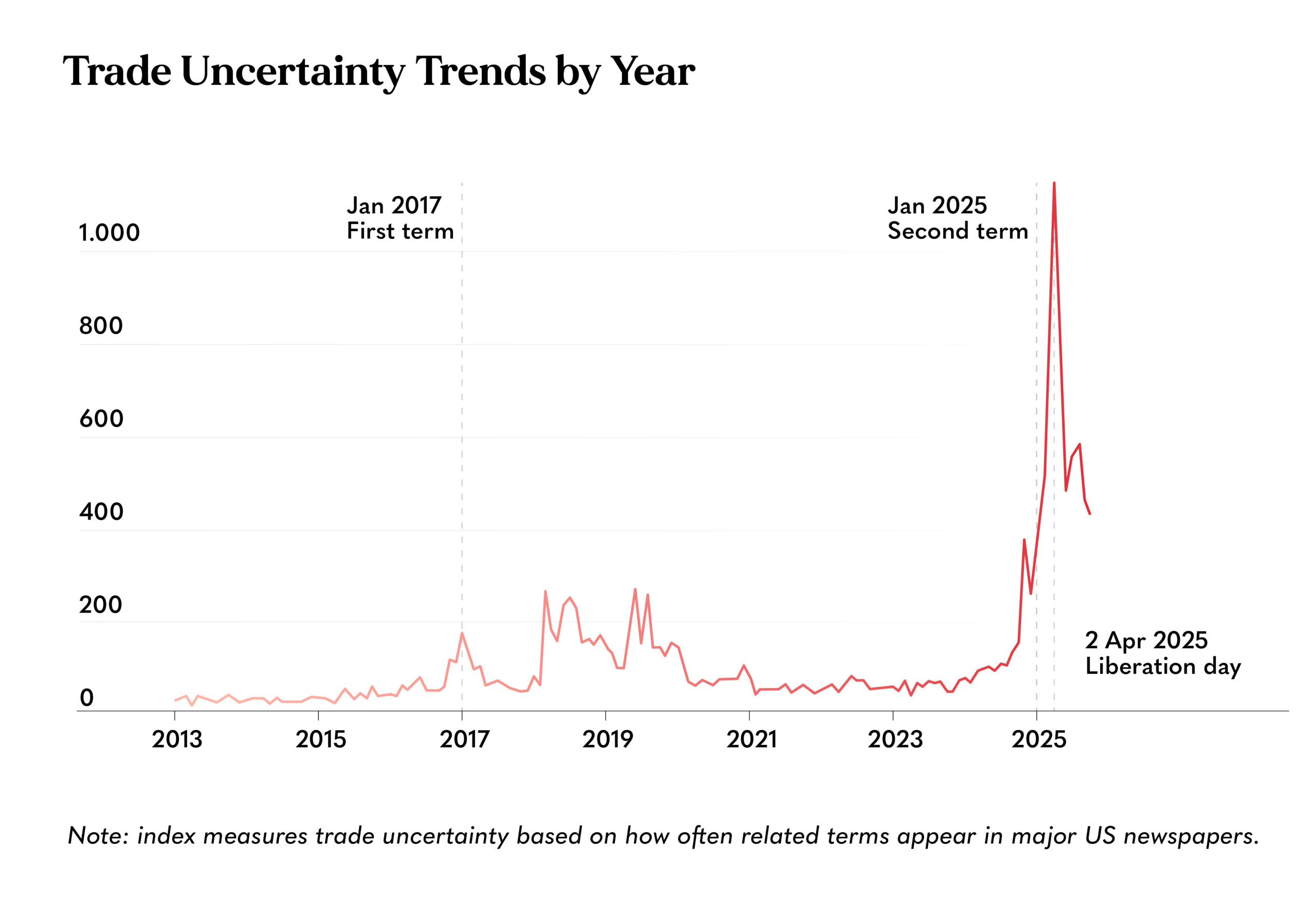

For eighty years, the international order built after World War II rested on a simple assumption: that the United States would broadly uphold it. That assumption is now gone. What’s taken its place is something harder to price, hedge, or predict—and markets are beginning to feel it.

Geoeconomic confrontation topped the World Economic Forum’s Global Risks Report for 2026, climbing eight positions in a single year. Half of the experts surveyed expect a turbulent or stormy world over the next two years, up 14 percentage points from the year before. The mechanisms through which instability travels into economies are well understood: supply chains are restructuring around political safety rather than cost efficiency, pushing up prices across industries; new trade agreements are being struck bilaterally outside multilateral institutions, creating a patchwork of rules that businesses cannot reliably plan around; and the share of G20 imports covered by tariffs has seen the largest increase in the history of WTO monitoring.

Sustained uncertainty alone—even without open conflict—functions as a structural drag on investment and growth, forcing companies to delay capital expenditures and investors to demand higher risk premiums. Beneath that, the numbers are sobering: global debt has reached $346 trillion, roughly 310% of global GDP, leaving governments with far less fiscal flexibility to absorb shocks than they had even five years ago. The AI investment boom, which contributed about 0.2 percentage points to the 2.2% U.S. economic growth in 2025, risks becoming a bubble if monetization disappoints, with a sudden drop potentially enough to tip the U.S. labor market into recession.

Three structural shifts define the new disorder. The prohibition on the use of force between states—one of the foundational pillars of the post-World War II order—has effectively been downgraded from an enforceable norm to an aspirational principle. The principle of self-determination of peoples, once a cornerstone of conflict resolution, is being quietly retired from peace negotiations. And the very concept of international law as a framework governing relations between states has disappeared from the official strategic doctrine of the world’s largest economy, substituted by an explicit assertion of the right to intervene wherever national interest dictates.

These are not isolated diplomatic incidents—they are precedents, and when the rules that once constrained the major powers’ behavior lose their teeth, the range of plausible scenarios widens dramatically. The order, in other words, has not collapsed: it has regressed. And regression, unlike collapse, is much harder to see coming. Until the check arrives.

Source: The Guardian

Imminent selection of global sources to dive deeper into the issue:

AI at Work: New Models Will Be Needed

Be ready to see AI scale and transform our business models. From Amazon to McKinsey, agentic AI and robotics are changing the game.

The AI revolution in productivity has not yet shown up in macroeconomic data, but the organizational disruption is already irreversible. U.S. productivity growth in 2025 came in at roughly 1.9%, just below the long-run historical average, and far short of the internet boom of the 1990s. AI contributed an estimated 0.25 to 0.5 percentage points of that. For all the noise, the numbers are modest. However, something structural is shifting beneath the surface that the aggregate data cannot yet capture.

McKinsey now counts 25,000 AI agents among its 60,000-strong workforce: over a third of its total headcount is non-human, up from a few thousand just eighteen months ago. Amazon plans to avoid hiring 160,000 people it would otherwise need by 2027, targeting 75% automation of its operations, with internal documents showing the company expects to sell twice as many products by 2033 without adding to its U.S. headcount.

What makes this moment different from previous waves of automation is the nature of the technology itself. Agentic AI—the defining shift of 2026—takes initiative. And now a human team of two to five people can already supervise a factory of 50 to 100 specialized agents running entire end-to-end business processes. IBM predicts that in the coming years, non-human identities will outnumber human users inside most large organizations. The question is no longer whether this changes business models. It is what the new models actually look like.

Source: Deloitte

The answer is beginning to come into focus across three dimensions. First, cost structures are being fundamentally repriced. When agents handle execution, the marginal cost of cognitive work trends toward the cost of compute, which falls continuously. Banks are already running mortgage and compliance processes with squads of agents. Insurers are reinventing claims and underwriting from scratch. This is a redesign of the entire process with humans positioned above the loop for strategic oversight. Second, customer relationships are being rewired. Consumers are already bypassing apps and search engines in favor of AI-native interfaces, and every company that owns a customer relationship now has the opportunity to become a personal concierge operating 24 hours a day, negotiating with other agents, learning continuously, and offering hyperpersonalized products across categories well beyond its traditional business. Third, proprietary data is becoming the decisive competitive asset. If today’s AI is, as one executive put it, “an intern with the internet in its pocket,” tomorrow’s edge will come from walled gardens of unique, consented, continuously refined data that the public internet cannot replicate.

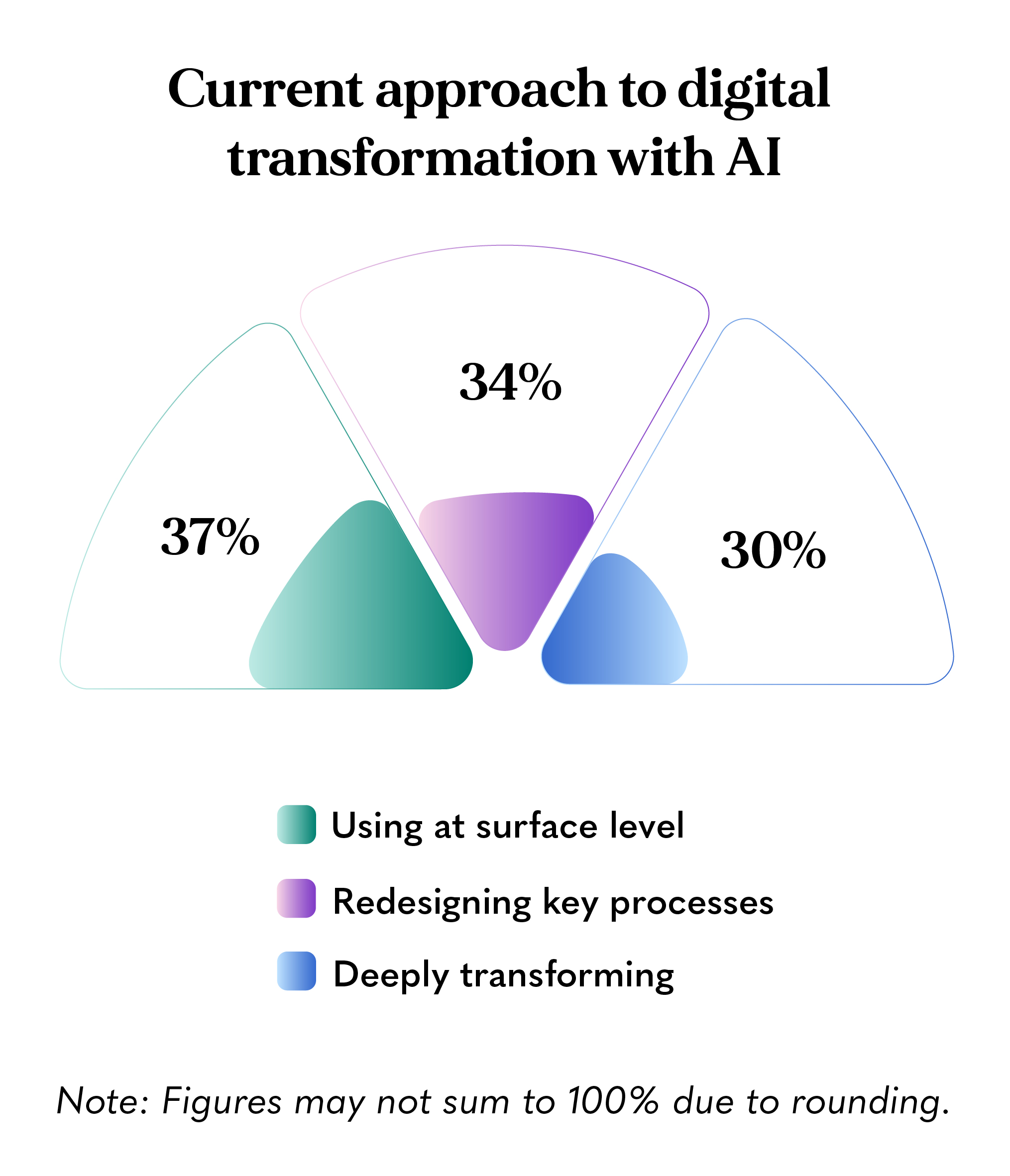

The gap between those who are genuinely transforming and those merely experimenting will become impossible to ignore in 2026. Gartner finds that only one in fifty AI investments delivers transformational value today. The reason is almost never the model, but the organization. Companies applying AI to individual tasks rather than redesigning entire workflows are leaving most of the value on the table. Workers, meanwhile, are caught in a revealing paradox that will define workplace dynamics this year: those most anxious about being replaced are also AI’s heaviest users, deploying it out of self-protection rather than genuine engagement, and producing activity, not impact.

The companies that will define the next decade are those that master orchestration: building flat networks of small, outcome-focused human/agent teams, redesigning workflows from scratch, and helping people understand their new role—as directors of machines, not executors of tasks.

Imminent selection of global sources to dive deeper into the issue:

Humans Out of the Loop?

From the U.S. Department of Transportation to Kyrgyzstan, AI in governance is becoming the biggest bet for many governments worldwide. How will this reshape our societies?

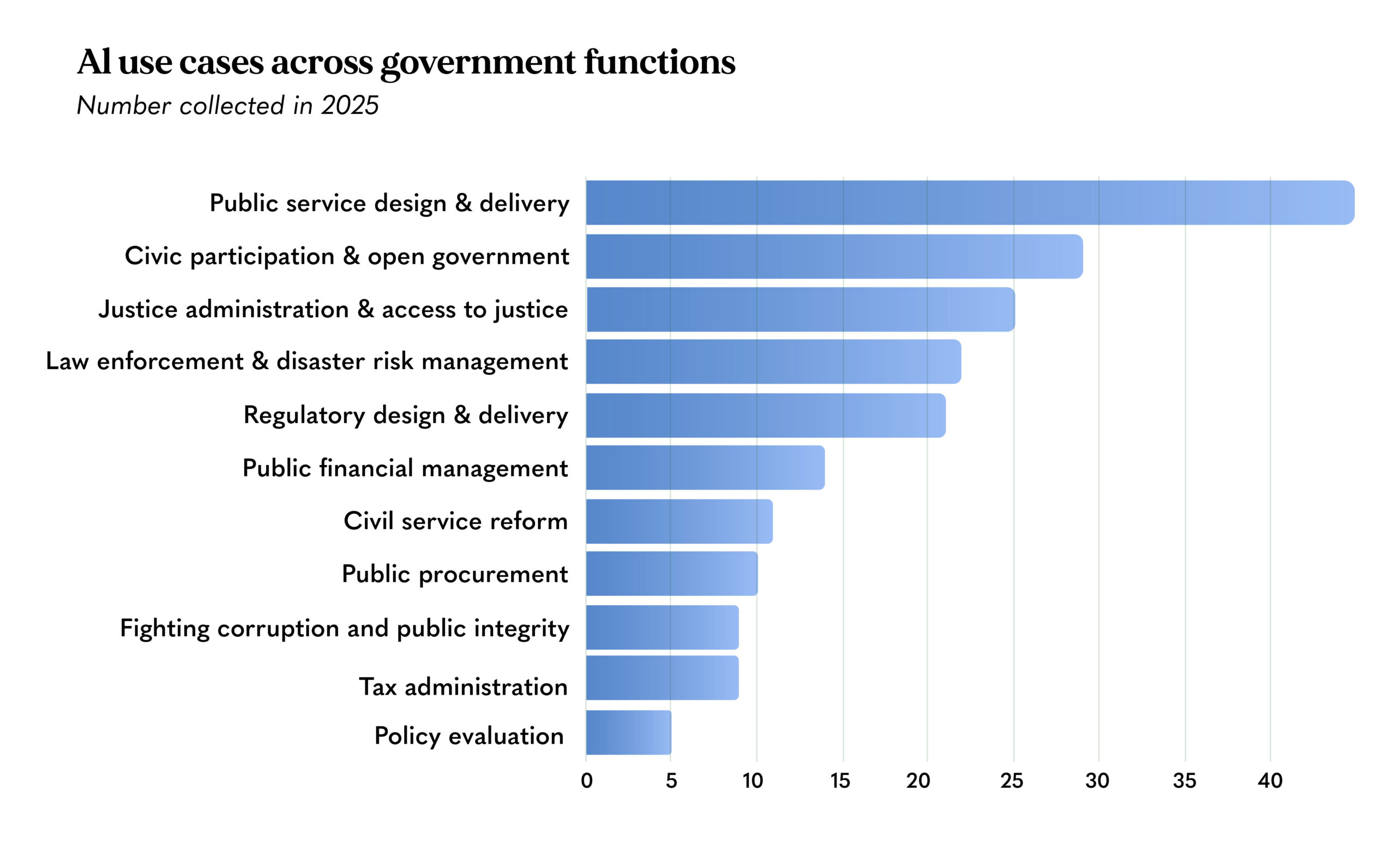

Something significant is happening. Quietly, across jurisdictions as diverse as Finland, Kyrgyzstan, Peru, and the United States, AI systems are taking over decisions that were once made by human beings: who qualifies for a pension, whether a tax inspection is warranted, how a safety regulation should be written, and which patient gets seen first. The question that defined 2025 was whether governments should adopt AI. The question defining 2026 is something harder: what happens when the human disappears from the decision entirely?

The examples are not hypothetical. In Kyrgyzstan, the national tax authority launched KEZET in January 2026—a system designed to replace human tax inspectors entirely, with 500 inspectors eliminated by May and another 500 by November, reducing the inspection workforce by roughly 30% within a year. In Finland, the government has proposed allowing AI to conduct the first triage of patients entering the public health system, replacing the nurse or doctor who currently assesses urgency and directs care—a reform arriving in the same legislative session as €170 million in healthcare cuts, timing that critics find impossible to ignore. In the United States, the Department of Transportation announced it would use Google Gemini to draft federal safety regulations for aircraft, pipelines, and trains.

What makes 2026 the inflection point is not that these experiments are new—it’s that they are becoming permanent, scaling fast, and happening without adequate governance frameworks in place. The EU AI Act‘s high-risk requirements take full effect in August, with penalties of up to €35 million or 7% of global turnover. Colorado’s AI Act comes online in June. California’s AI Transparency Act already took effect in January. China’s amended Cybersecurity Law, the first to explicitly reference AI, became enforceable on January 1st. For the first time, AI deployment at scale is colliding with serious enforcement—and the gap between what governments are deploying and what they can legally defend is widening by the week.

Research consistently shows that citizens accept AI-driven government decisions more readily when a human remains involved in the process. A 75% human, 25% AI ratio generates the greatest public acceptance, even outperforming fully human decisions. Yet the operational logic of agentic AI pushes in exactly the opposite direction: when systems execute thousands of micro-decisions per second, human review becomes a bottleneck, not a safeguard.

Source: OECD

The costs of getting this wrong are already visible. In Peru, an algorithm called SISFOH excluded over 81,000 elderly people from a poverty pension program between 2020 and 2025—not because they were not poor, but because the system measured household income rather than individual abandonment. Nobody caught it for five years. Meanwhile in New York, a municipal chatbot was shut down after providing consistently wrong information to citizens. These are previews of what happens when governance is automated faster than it is understood.

The deepest question 2026 is forcing into the open is not technical but political: who bears responsibility when an AI system governs badly? A court in Rome ruled in late 2025 that dismissing a worker whose role had been absorbed by AI was legally permissible—provided genuine organizational necessity could be demonstrated. A labor arbitration panel in Beijing ruled the opposite, finding that replacing a worker with AI constituted unlawful dismissal because choosing technology is a voluntary management decision, not an unforeseeable circumstance. Two jurisdictions, two opposite answers to the same question—revealing that the legal architecture for AI in governance is being written in real time, case by case, with no consensus in sight. The societies that navigate this best will not be those that resist AI in governance, nor those that embrace it fastest. They will be those which ask the right question early enough to matter: not “can AI make this decision?” but “should this decision ever be made without a human being accountable for it?” That distinction—between what is technically possible and what is democratically legitimate—is the defining governance challenge of 2026.

Imminent selection of global sources to dive deeper into the issue:

Demographic Winter Contracts the West

Where Is Value Created Today? Not in the West.

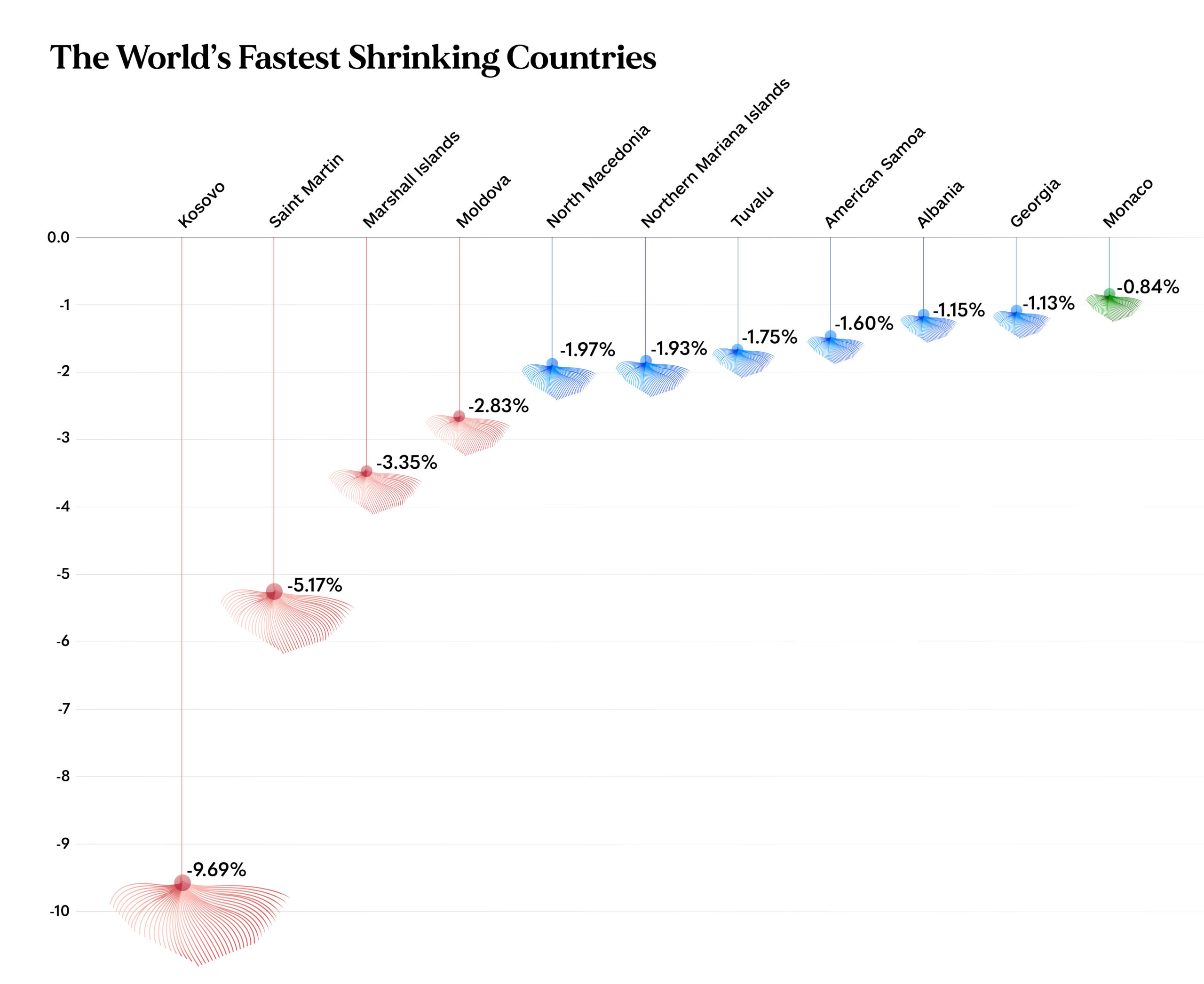

The most important economic story of the next 50 years is already written. Two-thirds of humanity now lives in countries where fertility has fallen below the replacement threshold. Italy‘s rate has reached 1.18 children per woman. South Korea‘s is 0.7. France, long Europe’s demographic exception, recorded more deaths than births in 2025 for the first time since World War II—a crossover that statisticians had not expected until 2035. The demographic winter that was once a long-run forecast is a present condition, and in 2026, its economic consequences are becoming impossible to ignore.

The mechanism is straightforward. Economic growth depends on having enough working-age people to produce, innovate, and fund the consumption of those who cannot work. That ratio is now deteriorating across virtually every advanced economy simultaneously. The share of the working-age population in western Europe, North America, Advanced Asia, and China peaked in 2010 and is in structural decline. By 2050, the global support ratio—working-age people per retiree—will fall to roughly four, down from over nine in 1997. In China, where a one-child policy combined with rapid aging, it will fall below one worker per retiree by 2080.

What makes 2026 the year to watch is that these trends are moving from abstract projections to visible operational problems. Companies across southern Europe already report more employees over 55 than under 35. Engineering vacancies go unfilled not because of pay but because the graduates simply do not exist in sufficient numbers. Italy lost a net 97,000 graduates aged 25 to 34 to emigration over the past decade, hollowing out the human capital base precisely when AI and green transition demand is rising fastest.

None of the policy responses developed so far has worked. No country where fertility has fallen below 1.9 has since recovered to replacement level: not Hungary, despite spending 6% of GDP on family programs; not South Korea, despite generous parental subsidies; not Scandinavia, despite some of the most generous parental leave systems in the world. The forces driving low fertility—housing costs, career timelines, cultural individualism, the economic incompatibility of early parenthood as currently organized—are structural, not contextual.

Source: VisualCapitalist

The part of this story that Western discourse consistently underweights is what is happening elsewhere. While first-wave economies age and shrink, the demographic center of gravity is shifting decisively toward sub-Saharan Africa, India, and parts of Emerging Asia. By 2050, later-wave regions will account for more than two-thirds of global hours worked and a growing share of global consumption. Nigeria alone will contribute more births than the whole of central, eastern, and western Europe combined within a generation. The question “where is value created?” is receiving a new answer in real time, and the answer is no longer automatically the West.

This bifurcation creates both an opportunity and a risk. The opportunity is a vast, young, growing labor force and consumer base in regions that have historically been peripheral to global economic governance. The risk is that 1.2 billion young people in developing countries will reach working age over the next fifteen years, while their economies are projected to generate only a third of the jobs needed to absorb them. This is a gap that, if unaddressed, translates into instability, irregular migration, and wasted human potential on a historic scale. The demographic winter and the demographic dividend are happening simultaneously, on opposite sides of the planet, and the world’s capacity to connect them will determine more about the shape of the global economy in 2040 than almost any other decision made today.

Imminent selection of global sources to dive deeper into the issue:

Africa’s Great Leap

From GDP growth to pivotal elections and emerging industries, the coming months will test Africa’s strategic weight in the global order.

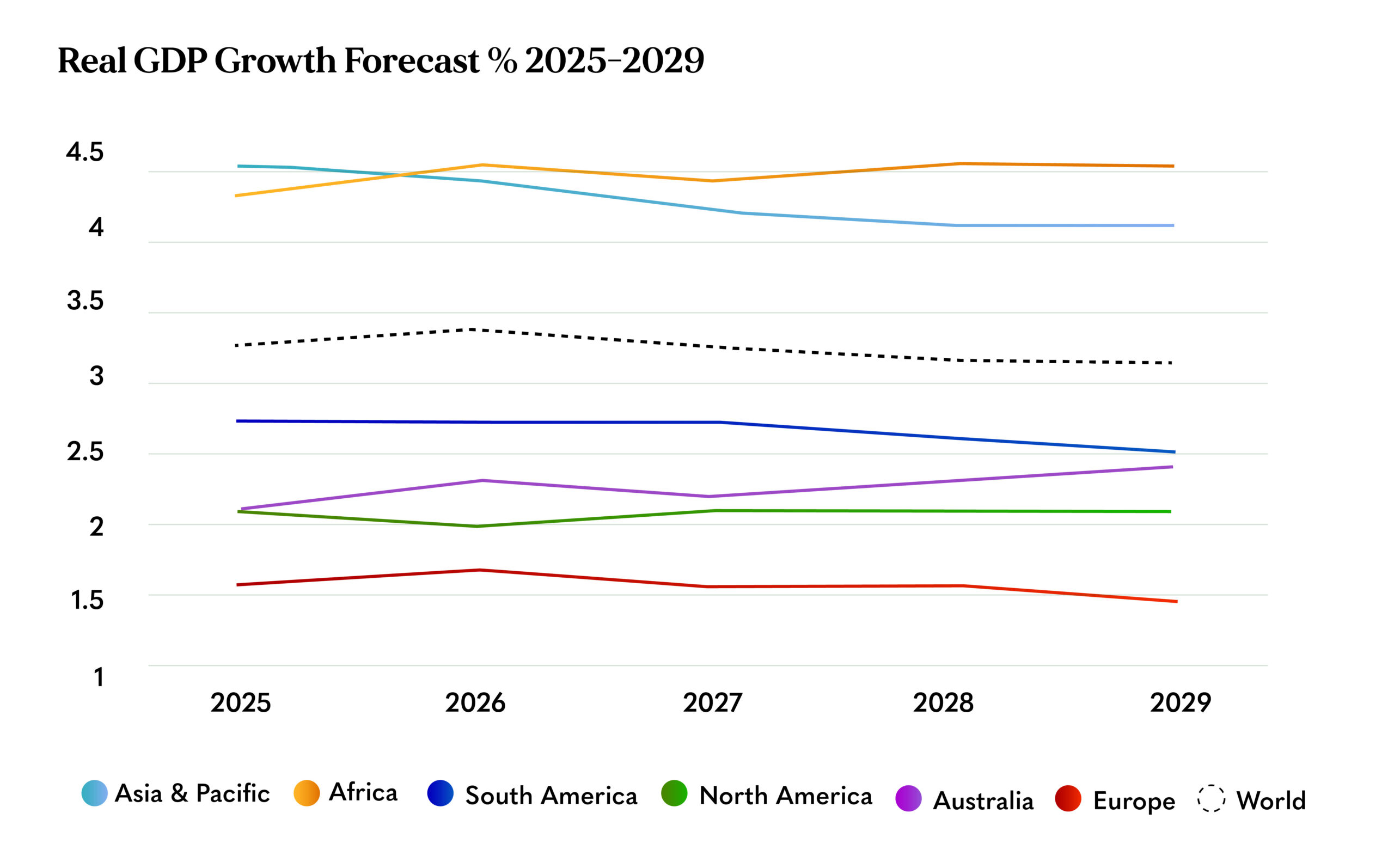

For the first time in modern history, Africa may grow faster than Asia in 2026. The IMF projects sub-Saharan Africa expanding by 4.3% while Asia slows to 4.1% as China’s engine decelerates after four decades of breakneck growth. It would be a statistical milestone, but it points to something more fundamental that no single data point can capture: the world is being rewritten, and Africa is no longer peripheral to that story.

The numbers are striking enough on their own. Eleven of the fifteen fastest-growing economies in the world in 2025 were African. East Africa is projected to grow at 5.8% in 2026, with Ethiopia above 10%. By 2050, one in four people on the planet will be African. The continent’s working-age population will exceed that of China and India combined. The same demographic dividend that Asia spent in the twentieth century, Africa is beginning to spend now—and unlike Asia, it is doing so in a world already reshaped by mobile technology, renewable energy, and the scramble for the critical minerals that power both.

What makes this moment different from previous “Africa Rising” narratives—and those have come and gone with depressing regularity since the commodity boom of the early 2000s—is that the structural conditions are shifting in ways that are harder to reverse. Africa’s critical minerals are suddenly the most strategically contested resources on earth. The lithium, cobalt, and copper embedded in the continent’s geology are not abstract future assets; they are the materials that every major economy needs right now to build batteries, data centers, and clean energy infrastructure. For the first time in a generation, African governments have genuine bargaining leverage.

The geopolitical environment is accelerating this shift. The USA’s withdrawal from USAID and dozens of multilateral commitments has effectively pulled away a pillar of Africa’s development architecture overnight, forcing a painful short-term reckoning, but one that could prove clarifying in the longer term. African governments that once oriented their strategies around Western aid flows are being pushed—and in some cases, choosing—to deepen intra-continental trade, court Gulf investors, expand South/South partnerships, and mobilize domestic resources more aggressively. The African Continental Free Trade Area, ratified by more than 50 countries, is the structural bet behind all of this: full implementation could add $650 billion to Africa’s economy by 2043 and lift 32 million people out of extreme poverty.

Source: Africa.com

Africa’s democratic and autocratic trajectories are diverging faster than at any point in recent decades, and 2026 is adding new data points to that divergence daily. The political calendar adds its own layer of complexity. Several of the continent’s most consequential countries—including Ethiopia, Zambia, the Gambia, and the Republic of Congo—head to the polls in 2026. Uganda has already set the tone: Museveni secured a seventh term in January in conditions that exposed the gap between a formal electoral process and genuine political legitimacy. That gap matters economically, not just morally. Countries where institutions hold credibility under pressure attract investment, sustain reform, and build the state capacity that turns commodity booms into lasting development. Those that don’t tend to recycle the same crises.

What remains uncertain is whether the decisions made under pressure in 2026—over mineral contracts, energy sequencing, electoral legitimacy, and trade implementation—will expand future options or quietly foreclose them. The demographics, the resources, and the geopolitical landspace are all moving in Africa’s favor. Whether that alignment becomes something durable is the issue worth watching—not because Africa needs the world’s attention, but because the world, increasingly, needs Africa to get this right.

Imminent selection of global sources to dive deeper into the issue:

LATAM’s Cultural Surge Is Underway

From the Super Bowl to the FIFA World Cup in Mexico, LAC is rising in influence—and Spanish may become the language of this new order.

On February 8, 2026, Bad Bunny took the stage at Levi’s Stadium for the Apple Music Super Bowl halftime show. No translator, no English-language crossover track, no concession to the assumption that global entertainment must arrive in one particular accent. Just Spanish, reggaeton, and 130 million viewers. It was the first time a Spanish-language artist had headlined the most-watched entertainment event in the United States. Latino culture is no longer knocking at the door of the global mainstream. It has moved in.

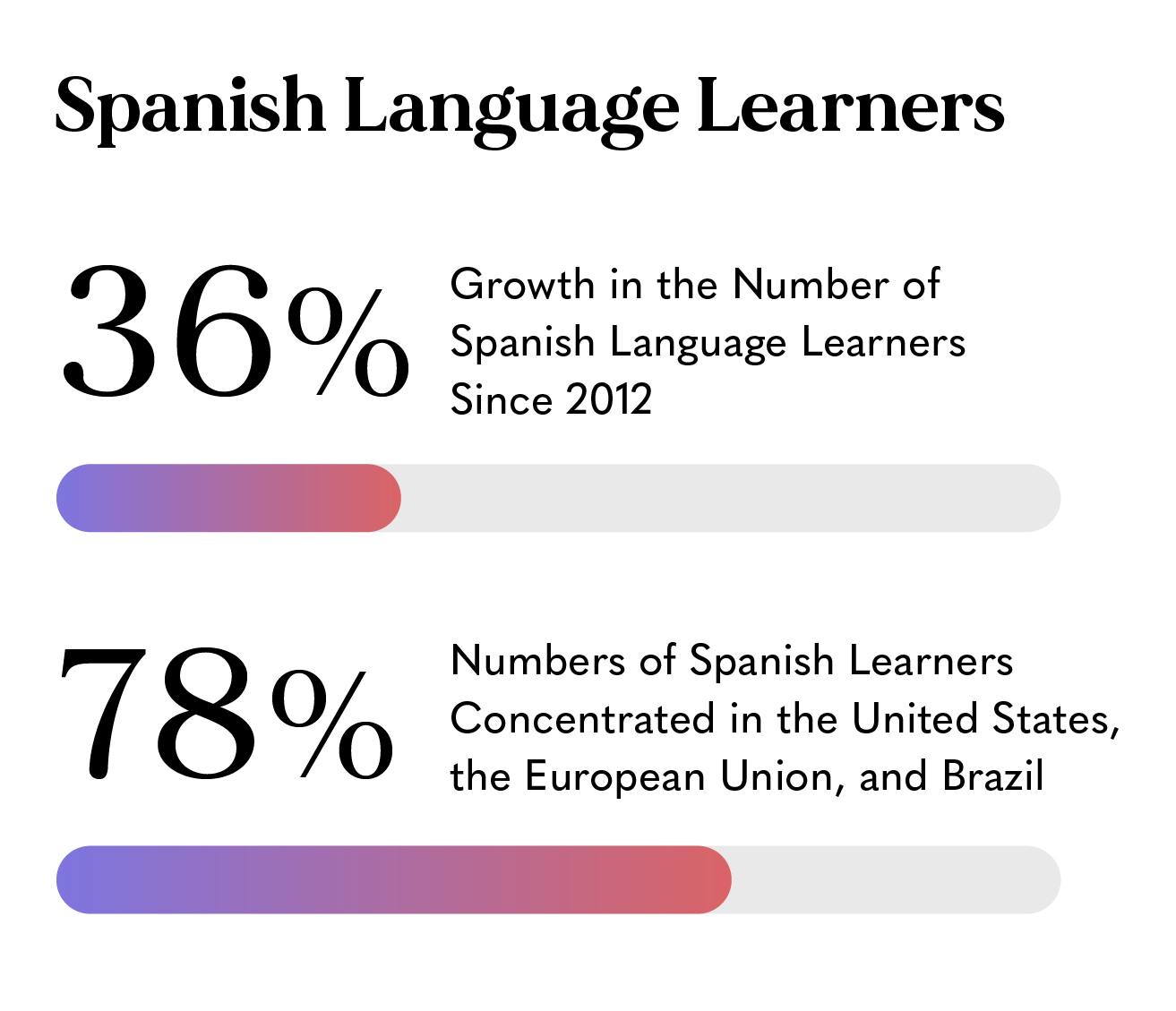

The numbers behind this moment are more structural than they appear. Spanish has now crossed the 600-million-speaker mark worldwide, with nearly 500 million native speakers making it the second-most spoken native language on earth. The United States alone will have close to 100 million Spanish speakers by 2050—a demographic reality so consequential that Spain’s King Felipe VI recently argued, without exaggeration, that the future global evolution of the language will depend largely on the American continent. When a Latin song goes viral, language-learning platforms report immediate surges in new Spanish learners. The tresillo rhythm of reggaeton has seeped into the production of British and American pop. The linguistic and aesthetic vocabulary of Latin America is becoming a shared global reference, not a niche export.

Streaming has been a great accelerant. Netflix pledged $1 billion in Mexican productions by 2028. Major adaptations of canonical Latin American novels have arrived on global platforms with international marketing budgets, and Spanish-language originals regularly rank in global top tens with 80 to 90% of their viewership coming from outside Spanish-speaking markets. What studios discovered is that language is not the barrier it once seemed. Meanwhile, VIX, TelevisaUnivision’s Spanish-language streaming platform, is projected to be the fastest-growing streaming service in the Americas.

This cultural surge did not arrive from nowhere. Latin America has always exported its imagination—what is different now is the breadth, the speed, and the economic weight behind it. The collective GDP of Spanish-speaking countries now represents over 6% of global output. The International Federation of the Phonographic Industry reports Latin America as one of the fastest-growing recorded music markets in the world, with Latin music generating $1.4 billion in U.S. sales alone in 2024. Books are following: Mariana Enríquez, Fernanda Melchor, and Cristina Rivera Garza are winning international prizes and being translated at scale. Visual art from the region has moved from the margins to the center of institutions in New York, London, and Madrid.

The soft-power dimension of all this is inseparable from harder geopolitical realities. Latin America enters 2026 as a region the world cannot afford to ignore: it holds 50–60% of the world’s lithium reserves, nearly 19% of proven global oil reserves, and copper deposits essential to every clean energy transition scenario. Seven countries, representing 52% of the region’s population, are undergoing presidential transitions this year. The EU-Mercosur trade agreement, more than two decades in the making, is moving toward formal implementation, creating what Oxford Economics called the largest free trade area in the world by population. Chilean equities are up 36% since October, the best-performing investable equity market globally. Argentina, Peru, and Colombia have followed. The region’s financial assets are among the best-performing in the world at the start of 2026, driven by commodity prices, a weaker dollar, and reform momentum.

Source: Instituto Cervantes

What 2026 is revealing is that culture, economics, and geopolitics in Latin America are no longer separate tracks that occasionally converge—they are the same story told from different angles. The FIFA World Cup comes to Mexico, the United States, and Canada later this year, and with it, the most-watched sporting event on earth will be hosted in the hemisphere where Spanish is already the dominant cultural language. That is not a coincidence. It is the shape of a shift that has been building for years, and now, in 2026, it is simply too large to misread.